Confidential Treatment Requested by Oportun Financial Corporation

Pursuant to 17 C.F.R. Section 200.83

OPORTUN FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. ORGANIZATION AND DESCRIPTION OF BUSINESS

Oportun Financial Corporation is the parent holding company of Oportun, Inc. Each are Delaware corporations and all business operations, other

than equity financing, take place at Oportun, Inc. and its subsidiaries. Oportun, Inc. was incorporated in August 2005 as Progress Financial Corporation, and the parent holding company was incorporated in August 2011 as Progreso Financiero Holdings,

Inc. In January 2015, the names of the two companies were changed to Oportun Financial Corporation and Oportun, Inc., respectively Oportun Financial Corporation and its subsidiaries are hereinafter referred to as the “Company.” The Company

is headquartered in San Carlos, California.

Doing business under the brand name “Oportun,” the Company is a

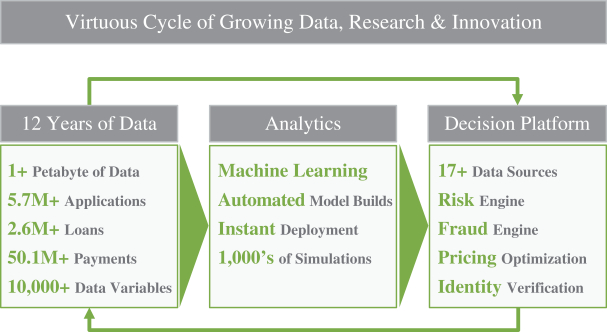

technology-powered and mission-driven provider of inclusive, affordable financial services to credit invisibles or mis-scored consumers. The Company provides small dollar, unsecured installment loans that are

affordably priced and that help customers establish a credit history. The Company has developed a proprietary lending platform that enables the Company to underwrite the risk of

low-to-moderate income customers that are credit invisible or mis-scored, leveraging data collected through the application process and data obtained from third-party

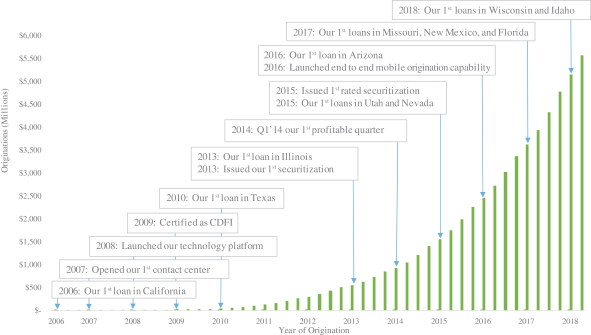

data providers, and a technology platform for application processing, loan accounting and servicing. The Company has been certified by the United States Department of the Treasury as a Community Development Financial Institution (“CDFI”)

since 2009.

The following wholly-owned subsidiaries of Oportun, Inc. in the United States have active operations as of June 30,

2018: PF Servicing, LLC, Oportun, LLC, Progreso Receivables Funding I, LLC, Progreso Receivables Funding II, LLC, Progreso Receivables Funding III, LLC, Oportun Funding I, LLC, Progreso Receivables VFN I, LLC, Oportun Funding III, LLC, Oportun

Funding IV, LLC, Oportun Funding V, LLC, Oportun Funding VI, LLC, Oportun Funding VII, LLC and Oportun Funding VIII, LLC. In addition, the Company also has the following wholly-owned subsidiaries which were inactive as of June 30, 2018: Oportun

Funding AFS I, LLC, Oportun Funding II, LLC, Oportun Funding A, LLC, Oportun Funding X, LLC and Oportun Funding XI, LLC.

Additionally, Oportun, Inc. has two wholly-owned subsidiaries in Mexico, PF Servicing, S. de R.L. de C.V and OPTNSVC Mexico, S. de R.L. de

C.V. (formerly PF Controladora, S. de R.L. de C.V.). These entities were incorporated under Mexican law in December 2010 with the purpose of establishing customer contact centers (PF Servicing) and providing administrative, support and other

services (OPTNSVC Mexico) to support operations in the United States. PF Servicing, S. de R.L. de C.V. commenced operations in August 2017.

As of June 30, 2018 the Company operated in California, Texas, Illinois, Utah, Nevada, Arizona, Missouri, New Mexico, Florida, Wisconsin and

Idaho. The Company commenced operations in New Mexico in April 2017, Florida in December 2017 and Wisconsin and Idaho in May 2018. Each state has consumer lending statutes that establish permitted loan pricing, fees and terms. State

agencies oversee the operations of licensees, including enforcement of applicable state statutes, compliance audits and annual reporting.

The Company uses securitization transactions, warehouse facilities and other forms of debt financing, as well as whole loan sales, to finance

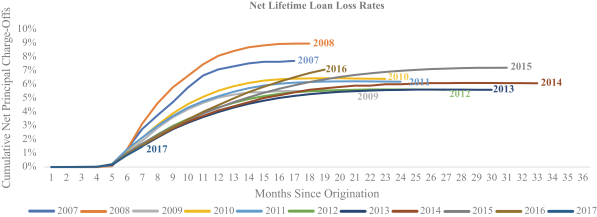

the principal amount of most of the loans it makes to its customers. As described in Note 9, some of the Company’s existing debt facilities contain debt covenants that require the Company not to exceed certain risk scores, and delinquency and

loss ratios in its loan portfolio. Breach of such covenants could cause the respective facility to enter into early amortization. Additionally, some of the Company’s borrowing facilities pay interest expense based on variable rates and an

increase in the underlying reference rate for such debt could increase the Company’s interest expense significantly. The Company monitors and is actively engaged in managing these risks. In order to continue to expand its operations and grow

its loan portfolio, the Company anticipates issuing additional debt and equity funding. Additional funding is dependent

F-8